Cheap Flights Need Cheap Fuel

What happens to US airline competition and airfare affordability after Spirit Airlines' collapse, and how exposed are remaining budget carriers to sustained high fuel prices?

When most people imagine an airline collapse, they picture a giant carrier going under after months of bad headlines. The airlines that actually disappear first will be the cheap ones, and the reason is jet fuel.

Most of us see ticket prices and assume they reflect the cost of running an airline. They don’t, mostly. Ticket prices reflect what each airline can charge while still making the math work, and that math is wildly different at Delta than it is at Spirit.

The cheap airlines run on a much thinner margin. When fuel jumps, the margin disappears, and the airline goes with it.

Why fuel decides everything

An airline’s biggest cost, after the planes themselves, is jet fuel. For a legacy carrier like United or Delta, fuel runs somewhere between a quarter and a third of operating cost. For an ultra-low-cost carrier like Spirit or Frontier, it runs closer to forty percent.

That difference matters because the budget airlines built their entire business on charging less than legacy airlines, by a lot. A $79 Spirit ticket from Newark to Fort Lauderdale wins customers away from a $250 United ticket on the same route. The trick is keeping every cost as low as humanly possible: stuffing more seats into each plane, charging for everything down to the carry-on, paying staff less, and praying fuel stays cheap.

When fuel goes from $3 a gallon to $4 a gallon, United absorbs it. The legacy carrier raises ticket prices a little, leans on futures contracts it bought last year, and keeps flying. Spirit can’t absorb it. A dollar of extra fuel cost on a $79 ticket eats the entire profit margin.

What’s happening right now

Spirit Airlines filed for bankruptcy. Frontier, Allegiant, and Sun Country are watching the same fuel prices and doing the same arithmetic.

The legacy carriers (United, Delta, American, Southwest) face the same fuel prices, but they have things the budget carriers don’t. Cash reserves to weather a year of bad fuel. Higher-fare business class and international routes that subsidize the economy seats. Existing fuel hedging contracts that lock in last year’s prices for a chunk of this year’s flying. A balance sheet that lets them borrow money to bridge the gap.

The budget carriers have planes, low ticket prices, and a customer base that came for cheap fares and will leave the moment fares go up.

Who actually gets hurt

About 40 million Americans fly on ultra-low-cost carriers each year. Most of them are families flying to see grandparents in another state, college students going home for break, retirees on fixed incomes flying to a vacation rental, and tourists going somewhere they couldn’t afford to visit on a $400 ticket.

For a lot of them, the cheap flight is the only flight. The route doesn’t exist on a legacy carrier, or it does but at a price that puts the trip out of reach. When the budget airline goes, the trip goes.

This hits hardest in places legacy carriers have mostly written off as too small to bother with. Rural Florida airports. Vacation towns in the Mountain West. Smaller Caribbean markets where the budget carriers were the only reason a route existed at all.

What happens when one goes under

When Spirit goes, every Spirit passenger needs to find another way to get where they’re going, and the legacy airlines flying those routes know it. Fares on those routes go up the next day, sometimes by 25 to 35 percent.

The damage to the surviving budget carriers takes longer to show up but matters more. Once financial markets decide the ultra-low-cost model is broken, Frontier can’t borrow money to ride out the fuel spike. Banks pull credit. Aircraft lessors get nervous about exposure to a sector everyone thinks is dying. Frontier and Allegiant (which admittedly, is running quite well at the moment), which were never as fragile as Spirit, end up with Spirit’s problem anyway. Nobody will lend them the cash they need to get through the year of bad fuel.

One bankruptcy flips the whole sector from “thin-margin but viable” to “structurally broken” in the eyes of the people who finance airlines, and the rest follow.

The rescue that probably won’t come

The clearest way to keep a competitive market alive is the federal government writing a check. About $2.5 billion of bridge financing, by our analysis, would keep at least two ultra-low-cost carriers operating through the fuel crisis and preserve the cheap-fare segment.

That’s the kind of bailout Washington did for the entire airline industry during COVID. The political appetite to do it again, specifically for the cheap airlines, is essentially zero. The legacy carriers have a lobbying operation in Washington that the budget carriers don’t. They will quietly argue the market should sort itself out, and that argument will probably win.

So the cheap-airline collapse, if it comes, comes with no rescue.

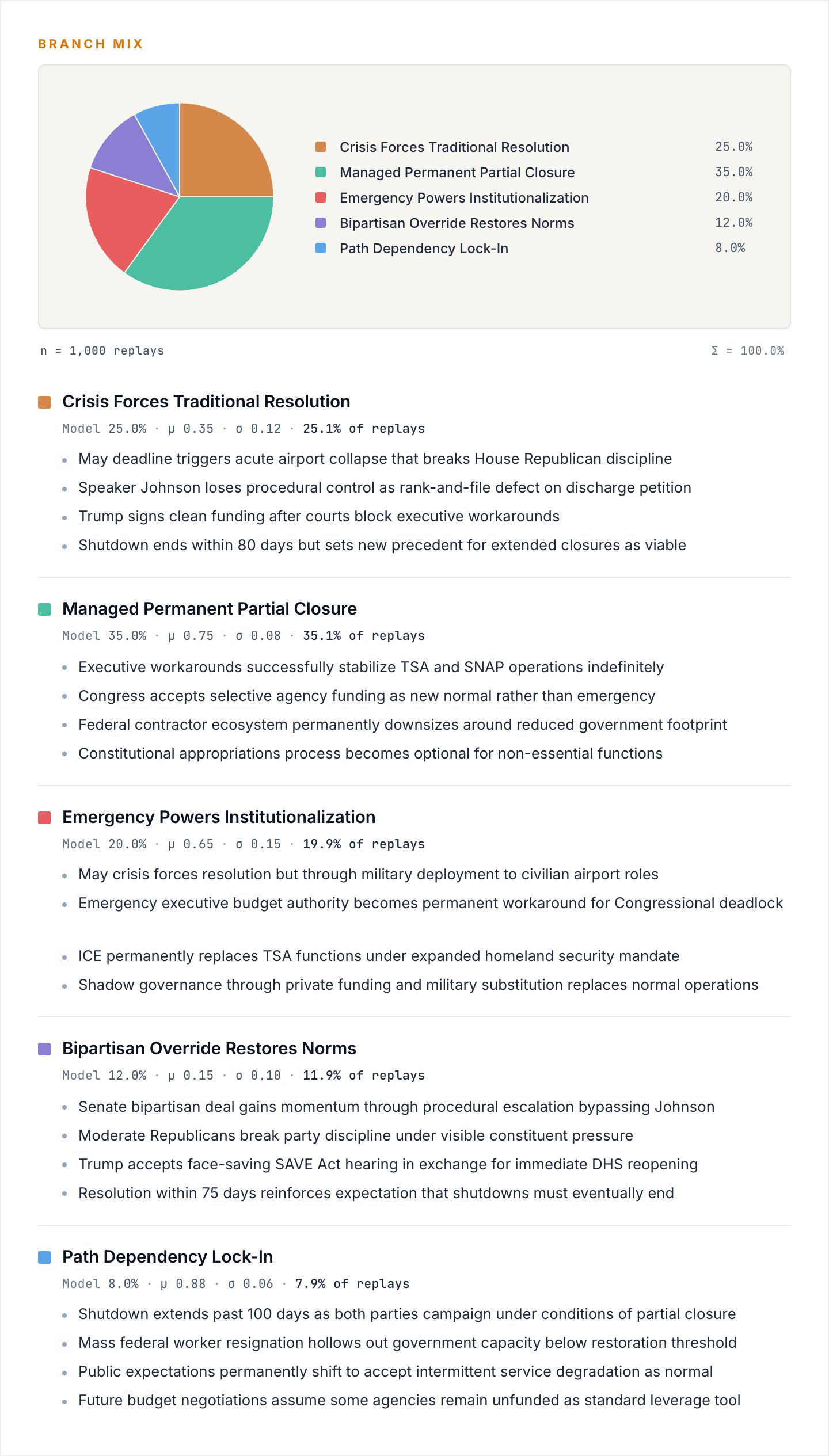

What the numbers say

The model is not friendly to budget travel. About two in five scenarios end with the ultra-low-cost segment essentially eliminated and average fares on former budget routes 25 to 35 percent higher. Roughly one in four end with one budget carrier (most likely Frontier) pivoting to a slightly more expensive but still cheaper-than-legacy model, the way JetBlue did, preserving some price competition but not the $79 fare.

Only about one in six scenarios end well. Fuel prices fall fast, the budget carriers ride it out, the market structure survives.

The rest sit in the middle. Several budget carriers fail, fares rise but not catastrophically, and the cheap-flight option mostly disappears outside the busiest corridors.

The $79 transcontinental flight stops being a thing across nearly every path, even the soft ones. That price point is what the fuel math is killing.

What happens next

We think Spirit does not reorganize and emerge as a viable airline. What comes out of bankruptcy court will be a smaller asset shell that gets bought for the route slots and the planes. The Spirit brand stops flying within twelve months.

Frontier survives, but not as an ultra-low-cost carrier. Sometime in the next eighteen months, Frontier announces a “premium economy” cabin or a rebrand toward a JetBlue-style mid-market product. The CFO will frame it as evolution. It is the abandonment of the segment.

Allegiant in trouble. Allegiant’s business model depends on flying older, fuel-thirsty planes on infrequent routes to vacation destinations, which is the worst possible exposure to a sustained fuel spike. We give Allegiant a coin-flip chance of being another domino, with Sun Country a smaller but real risk behind them.

The legacy carriers move into former Spirit markets within weeks of the bankruptcy filing. Starting fares on those routes settle 25 to 35 percent above where Spirit was, and stay there. The fares do not come back down when fuel does, because the competitive pressure that kept them low is gone.

No federal rescue arrives. There may be a hearing or a bipartisan letter. There will not be $2.5 billion of budget-carrier bridge financing.

The $79 transcontinental fare is gone by the end of 2026 and does not return.

We could be wrong about any individual piece of this. A Hormuz settlement could collapse fuel prices and stall the whole scenario. A Frontier-Allegiant defensive merger could preserve a single weakened budget competitor longer than we expect. We don’t think any of that flips the basic shape of where this is heading. It changes the timing.

A permanent compression of who gets to fly affordably in America, finished by the end of 2027.

What to watch

Frontier’s quarterly guidance on fuel costs. Frontier is the largest surviving budget carrier and the one most likely to pivot. When their CFO starts using phrases like “premium economy” or “differentiated cabin product,” the ultra-low-cost model is over even if the company isn’t.

Credit downgrades on the remaining budget carriers. Markets price the cascade before it happens. Watch for Allegiant or Sun Country debt getting downgraded with language about “elevated refinancing risk.”

Legacy carrier route announcements into former Spirit cities. Within weeks of Spirit’s bankruptcy, United and Delta will announce new routes into markets Spirit served. The starting fares on those routes will be substantially higher than Spirit charged, and they will not come back down.

Whether anyone in Washington proposes a budget-carrier-specific bailout. The window for designed intervention is narrow, probably six months, and closes the moment the legacy carriers fully absorb Spirit’s market share. After that, the consolidation is locked in and...